Table of Contents

Table of Contents

Simple vs Compound Interest: What’s the Real Difference?

Simple vs compound interest is one of the most important concepts in personal finance. Understanding the difference between simple vs compound interest helps investors evaluate savings accounts, loans, and long-term investments.

Interest determines how money grows over time when you invest—or how much borrowing money can cost. While both simple interest and compound interest calculate returns based on a percentage rate, the way interest accumulates is fundamentally different.

Simple interest grows at a steady, predictable pace, while compound interest accelerates growth by allowing interest to earn additional interest over time.

Understanding simple vs compound interest is essential for making smarter financial decisions about saving, investing, and borrowing.

Key Takeaways

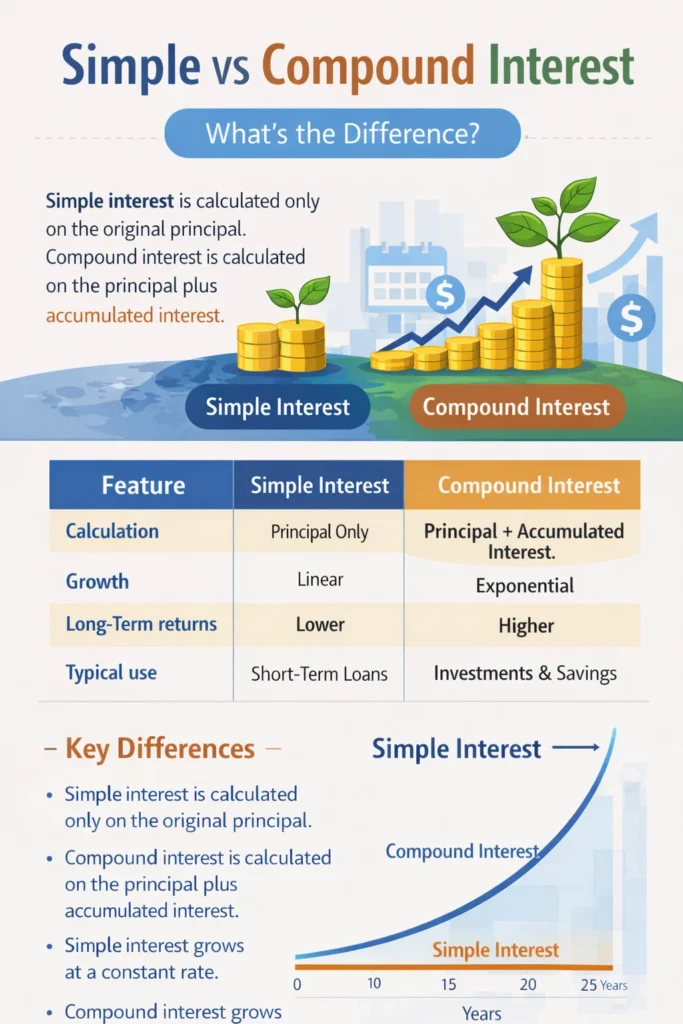

- Simple interest is calculated only on the original principal.

- Compound interest is calculated on the principal plus accumulated interest.

- Over long periods, compound interest produces significantly higher returns.

- Most investments and savings accounts rely on compound interest.

What Is Interest?

Interest is the cost of borrowing money or the reward for lending or investing money.

When individuals borrow money—through loans, mortgages, or credit cards—they pay interest to the lender. On the other hand, when people deposit money in savings accounts or invest in financial assets, they earn interest as compensation for allowing their money to be used.

Interest is usually expressed as a percentage rate applied to the principal, which is the original amount borrowed or invested.

There are several ways to calculate interest, but the two most common methods are simple interest and compound interest.

What Is Simple Interest?

Simple interest is calculated only on the original principal amount.

Unlike compound interest, simple interest does not consider previously accumulated interest. Because of this, the interest earned or paid remains constant throughout the entire period.

This makes simple interest predictable and easy to calculate.

Simple interest is commonly used in:

short-term personal loans

auto loans

some bonds

certain installment loans

Because interest does not compound, growth follows a linear pattern, meaning the balance increases by the same amount each year.

Simple Interest Formula

I = P \times r \times t

Where:

- P = principal (initial amount)

- r = interest rate

- t = time period

Example of Simple Interest

Suppose you invest $1,000 at a 5% annual simple interest rate for five years.

Annual interest:

$1,000 × 5% = $50

Because interest is calculated only on the original principal, the amount earned each year remains constant.

Over five years:

$50 × 5 = $250

Final balance:

$1,000 + $250 = $1,250

This illustrates how simple interest grows steadily over time.

What Is Compound Interest?

Compound interest is calculated on both the principal and the accumulated interest from previous periods.

This means that interest begins to generate additional interest. Over time, this creates an accelerating growth effect known as compounding.

Because of this powerful mechanism, compound interest is often referred to as “interest on interest.”

Most long-term financial products rely on compound interest, including:

- savings accounts

- investment portfolios

- retirement funds

- mutual funds

index funds

Compound Interest Formula

FV=P(1+r)tFV = P(1+r)^tFV=P(1+r)t

PVPVPV

r (%)r\,(\%)r(%)

Where:

- P = principal

- r = interest rate

t = number of periods

Example of Compound Interest

Using the same scenario:

Initial investment: $1,000

Interest rate: 5% annually

Time: 5 years

Year 1

$1,000 → $1,050

Year 2

$1,050 → $1,102.50

Year 3

$1,102.50 → $1,157.63

Year 4

$1,157.63 → $1,215.51

Year 5

$1,215.51 → $1,276.28

Compared with simple interest ($1,250), compound interest produces higher returns over time.

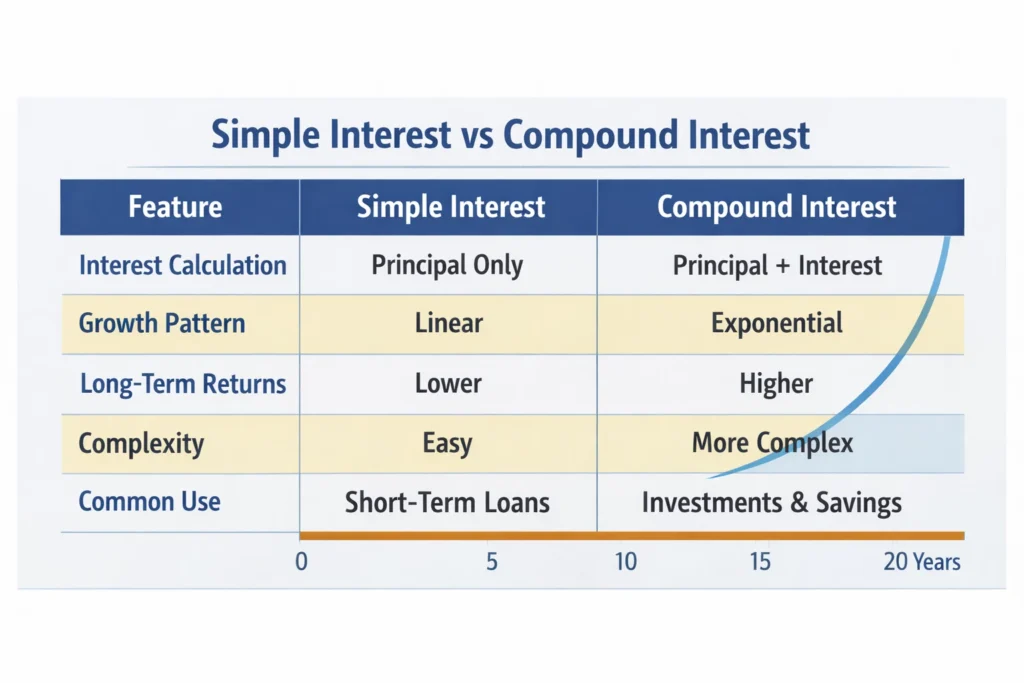

Simple vs Compound Interest: Key Differences

The key difference between simple vs compound interest lies in how interest accumulates over time.

Feature | Simple Interest | Compound Interest |

Interest calculation | Principal only | Principal + accumulated interest |

Growth pattern | Linear | Exponential |

Long-term returns | Lower | Higher |

Complexity | Simple | More complex |

Common use | Short-term loans | Investments and savings |

Over long periods, the gap between simple and compound interest becomes significantly larger.

Try the Compound Interest Calculator

- initial investment

- monthly contributions

- interest rate

- investment horizon

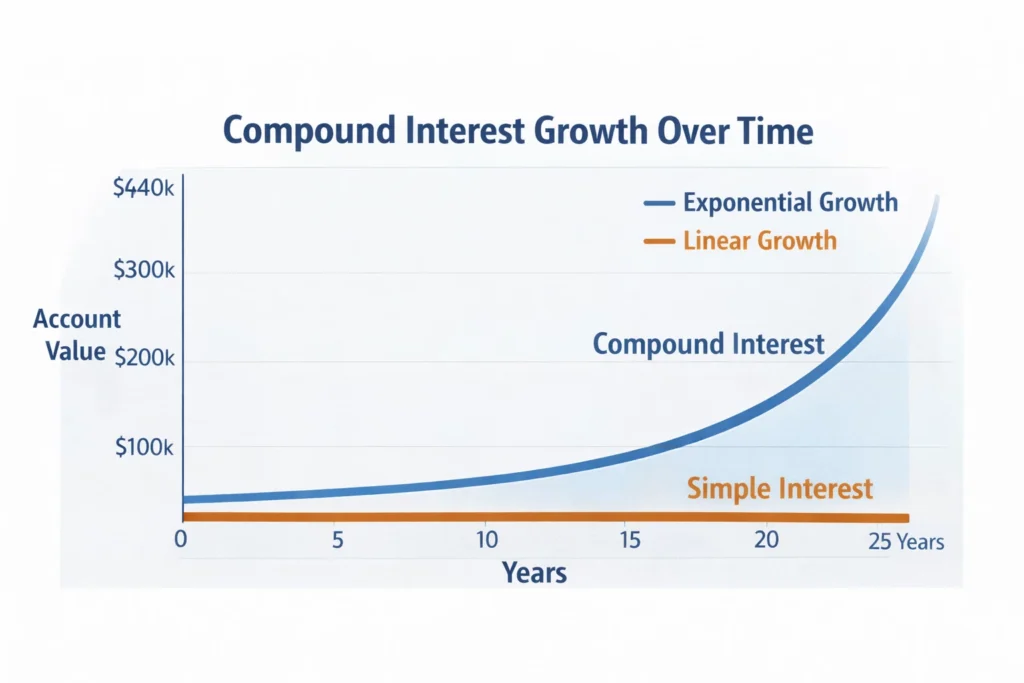

Why Compound Interest Is So Powerful

Compound interest becomes extremely powerful over long periods.

Each compounding cycle increases the base amount used for the next calculation. As a result, the growth curve becomes progressively steeper.

For long-term investors, compound interest is one of the most powerful mechanisms for building wealth.

Albert Einstein reportedly referred to compound interest as “the eighth wonder of the world.”

The Role of Time in Compounding

Time is one of the most important variables affecting compound interest.

Example:

Investing $5,000 at 7% annually

After 10 years → about $9,835

After 20 years → about $19,348

After 30 years → about $38,061

Even without additional contributions, the investment grows dramatically due to compounding.

This is why financial advisors often emphasize starting to invest as early as possible.

Real-World Examples of Compound Interest

Compound interest is widely used across financial systems.

Savings Accounts

Banks often compound interest daily or monthly, allowing deposits to grow faster.

Investment Portfolios

Stocks, bonds, ETFs, and mutual funds benefit from reinvested earnings.

Retirement Accounts

Long-term retirement vehicles rely heavily on compound interest over decades.

Compound Interest and Debt

While compound interest benefits investors, it can also increase borrowing costs.

Credit cards are a common example. Many credit card balances compound interest daily, meaning unpaid balances can grow rapidly.

Because of this, financial experts recommend paying off high-interest debt as quickly as possible.

Understanding simple vs compound interest helps borrowers avoid expensive financial mistakes.

Why Understanding Interest Matters

Many financial decisions involve interest, yet many people underestimate its long-term effects.

Understanding simple vs compound interest helps individuals:

- compare financial products

- evaluate loan costs

- maximize investment growth

- plan long-term financial goals

Financial literacy begins with understanding fundamental concepts such as interest and compounding.

Final Thoughts

The difference between simple vs compound interest may seem small at first, but over time it leads to dramatically different financial outcomes.

Simple interest produces steady and predictable growth based only on the principal.

Compound interest, however, allows interest to accumulate on both the principal and previously earned interest, creating exponential growth.

For investors, compound interest is one of the most powerful tools for building long-term wealth.

For borrowers, understanding compounding can help prevent costly debt.

The most important lesson is simple: the earlier you start investing, the stronger the power of compounding becomes.

Frequently Asked Questions

What is the difference between simple vs compound interest?

Simple interest is calculated only on the original principal, while compound interest is calculated on both the principal and accumulated interest.

Which is better: simple or compound interest?

For investors, compound interest is generally better because it allows investments to grow faster over time.

Do banks use compound interest?

Yes. Most savings accounts and investment products use compound interest, typically compounded daily or monthly.

Why is compound interest important for investing?

Compound interest allows investment returns to generate additional returns, accelerating wealth accumulation over time.